I CAN ASSIST IN 35+ STATES

My expertise

I've dedicated my entire adult career to the mortgage & life insurance industry. 20+ years. I can do all loans, but the niche I love is "creative financing". I primarily work with business owners, entrepreneurs and investors that cannot, or do not want to go the "conventional" financing route, full documentation, etc. I appreciate and love the challenge in structuring these loans. Whether asset based, alt-doc, no doc, or anywhere in between, you've chosen the right growth partner. Let's get started!

I am also the CEO of The Benefit Store [click here]

E Mortgage Capital, Inc. is one of the largest full-service mortgage companies in the country that offers extensive options for residential, commercial, and business financing, with quick service, unmatched communication, and leading rates.

We work with over 135 lenders.

PREVIEW OUR LIST OF SERVICES

Alternative Documentation Loans & Real Estate Investing

THERE ARE MORE ALTERNATIVE FINANCE OPTIONS TODAY THAN EVER BEFORE!

If you're a business owner, 1099 contractor, or real estate investor that's looking for unconventional, or alt-doc lending options that don't require tax returns, I can help. Residential, Commercial, Business financing available in 35+ states.

✅ Investor Loans (Debt Service Coverage Ratio)

✅ Delayed Financing (Get Funds Back After Paying Cash)

✅ Doc-Less Financing (Easy As Sunday Morning)

✅ Bank Statement Loans (12 - 24 Months. No Taxes)

✅ Asset Depletion (Leverage Liquid Assets As Income)

✅ Can be closed in an LLC (Limited Liability Company)

This is a great opportunity for those looking to get started with rental properties, or have a means to purchase your next primary or second home without having to worry about taxable income.

Wealth Accumulation, Preservation,

& Protection

MY TEAM AND I ARE EXPERTS AT STRUCTURING TAX ADVANTAGED VEHICLES TO HELP YOU MEET YOUR FINANCIAL GOALS!

✅ Executive Bonus Plans

✅ Key Man Insurance

✅ 401K | IRA Conversions & Alternatives

✅ 529 College Savings Plan Alternative

✅ Guaranteed Income For Life Fixed Indexed Annuities

✅ Be Your Own Bank (Avoid Bank Interest + Gain Compound Interest)

Workers Comp Risk Management Platform

Save 20% - 40% on your workers comp premiums and claims. Significantly reduce Employee Turnover, Absenteeism, while increasing Productivity.

We specialize in the utilization and administration of the Wellness Integrated Medical Plan Expense Reimbursement (WIMPER) program. This program utilizes concise tax codes to install our platform in a way that there are "zero additional net out-of-pocket costs" to the employer or the employee.

Wealth Accumulation, Preservation,

& Protection

MY TEAM AND I ARE EXPERTS AT STRUCTURING TAX ADVANTAGED VEHICLES TO HELP YOU MEET YOUR FINANCIAL GOALS!

✅ Executive Bonus Plans

✅ Key Man Insurance

✅ 401K | IRA Conversions & Alternatives

✅ 529 College Savings Plan Alternative

✅ Guaranteed Income For Life Fixed Indexed Annuities

✅ Be Your Own Bank (Avoid Bank Interest + Gain Compound Interest)

ALTERNATIVE DOCUMENTATION LENDING

Approved In As Little As 15 Minutes

IT’S EASY WHEN YOU HAVE AN INITIAL APPROVAL

Want to feel good about making a strong offer on your dream home?

Get an initial approval for your loan almost instantly when you work with independent mortgage professionals like us. Our cutting-edge process lets us do what big banks and retail lenders can’t and give you an initial loan approval in as little as 15 minutes — even on the weekends!

You’ll also enjoy greater transparency so you can gather any paperwork you need ahead of time and make sure your loan goes through as smoothly as possible.

Investor Flex Loans

(Debt Service Coverage Ratio)

THE TIME TO EXPAND YOUR PORTFOLIO IS NOW!

We have a quick and easy way to purchase more investment properties. Our Debt-Service Coverage Ratio (DSCR) loan allows you to qualify for investment properties based on the prospective monthly rental income.

✅ Finance up to 20 properties

✅ Loan amounts up to $3M

✅ Eligible for short-term and long-term rentals

✅ Low reserves requirement (as little as 3 months)

✅ Can be closed in an LLC (Limited Liability Company)

This is a great opportunity for those looking to get started with rental properties, as well as those looking to grow.

Bank Statement Loans

PUT BANK STATEMENT LOANS TO WORK FOR YOU

If you’re self-employed, gathering income documents or tax transcripts for a mortgage application can be a real hassle. That’s why we offer Bank Statement Loans – where you can simply provide bank statements to qualify for loans up to $3.5M.

✅ Min FICO credit score of 620

✅ No mortgage insurance required

✅ Available on primary, second home and investment properties

✅ As little as 6 months reserves required

Asset Depletion Loans

LEVERAGE YOUR LIQUID ASSETS AS INCOME FOR QUALIFYING

An Asset Depletion Loan allows you to use the current cash value of your liquid assets – instead of traditional income sources such as pay stubs and tax returns – to demonstrate your ability to afford timely mortgage payments. This program is ideal for borrowers who have adequate liquid assets but lack traditional employment and/or methods of income verification.

How It Works

With an Asset Depletion Loan, your income is calculated by dividing your total liquid assets over 360 months. Assets that qualify as liquid assets include retirement accounts, investment accounts, checking accounts, savings accounts, stocks, bonds, CDs, etc. You can use 100 percent of your cash and non-retirement investment accounts in calculating your total liquid assets if you are over the age of 59.5, and 70 percent if you are under 59.5.

✅ Non-retired and retired borrowers are eligible

✅ Not penalized on rates for leveraging your assets

✅ You can couple asset depletion income with other forms of income

✅ 75% maximum loan-to-value ratio (LTV)

✅ All occupancy and collateral types are allowed

✅ Up to 50% debt-to-income ratio (for FICO scores >650)

Delayed Financing Loans

GET YOUR MONEY OUT OF YOUR HOME AND INTO YOUR SAVINGS

✅ Refinance immediately after purchase.

✅ Close your loan in an average of 20 days.

✅ Free up your cash for other expenses or investments.

Doc-Less Loans

GET A FASTER, EASIER MORTGAGE OR REFINANCE WITHOUT THE HASSLE OF GATHERING FINANCIAL DOCUMENTS

Here’s how it works.

✅ You simply e-sign your loan documents

✅ We verify your income, assets and tax returns

✅ We notify you when your loan is approved

Adjustable Rate Mortgages

TODAY'S ADJUSTABLE-RATE MORTGAGES ARE A LOT DIFFERENT THAN THEY WERE IN THE PAST

And they may be the best choice for your purchase or refinance:

ARMs are smarter

✅ Most people only stay in their mortgage for 5 to 7 years. Why not go for the lower rate?

✅ With an ARM, more of your payment goes toward the principal, so you pay down your mortgage faster

ARMs are often safer

✅ ARMs no longer feature pre-payment penalties, so you can easily refinance

ARMs can save you money

✅ A lower rate means a lower payment, which means more cash in your pocket each month

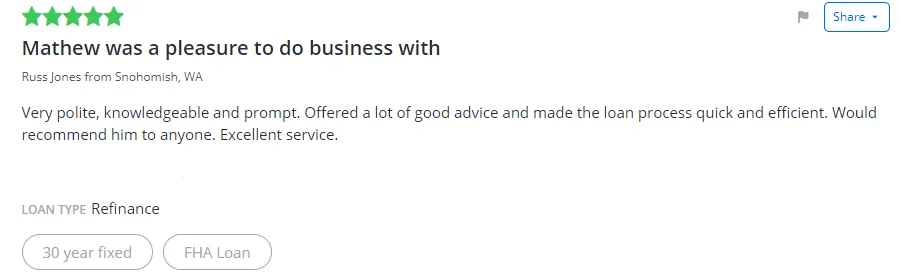

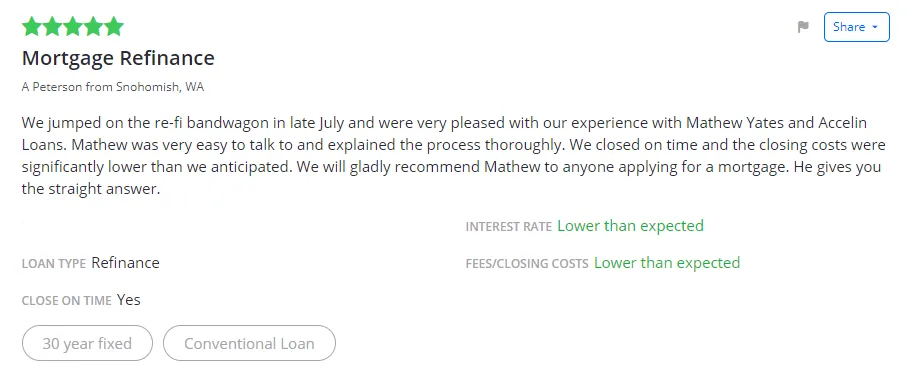

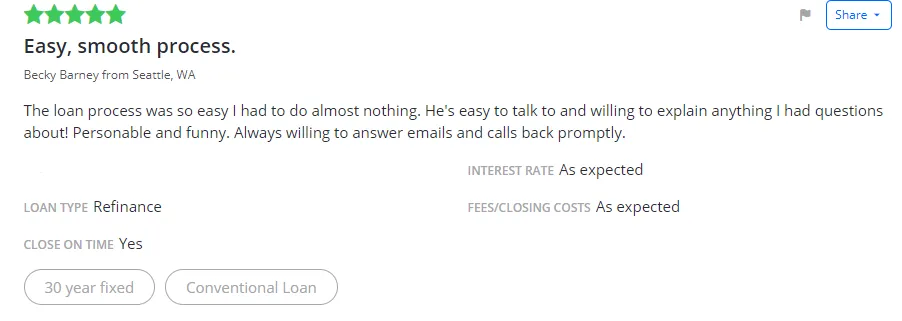

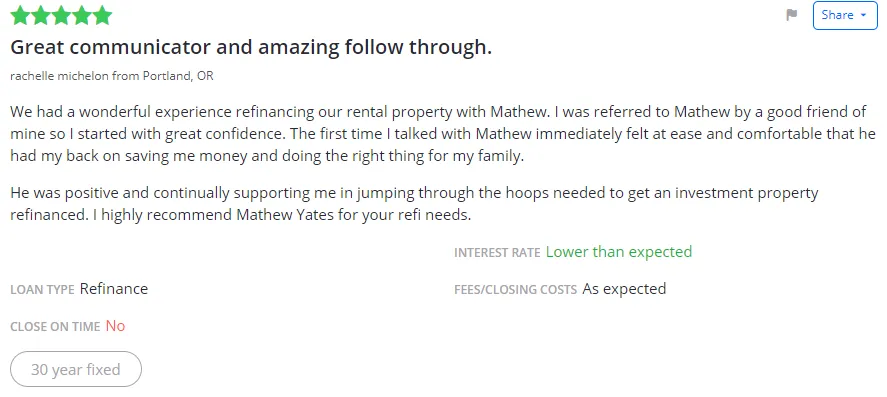

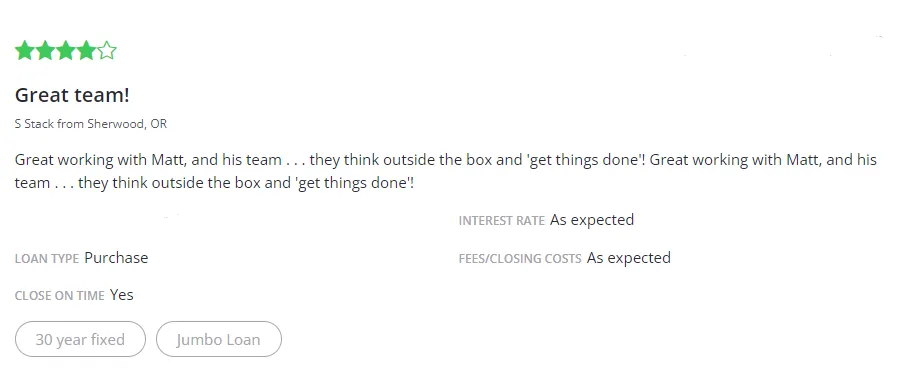

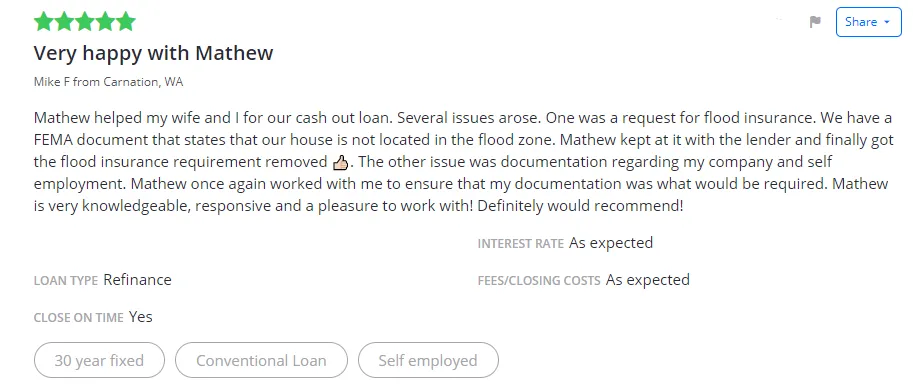

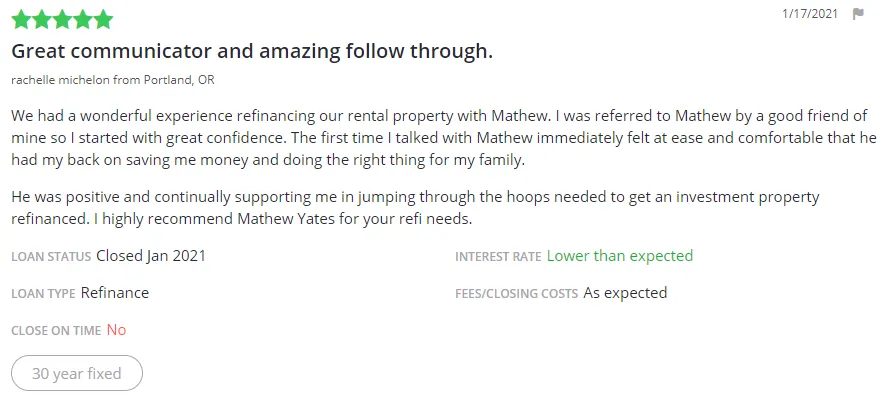

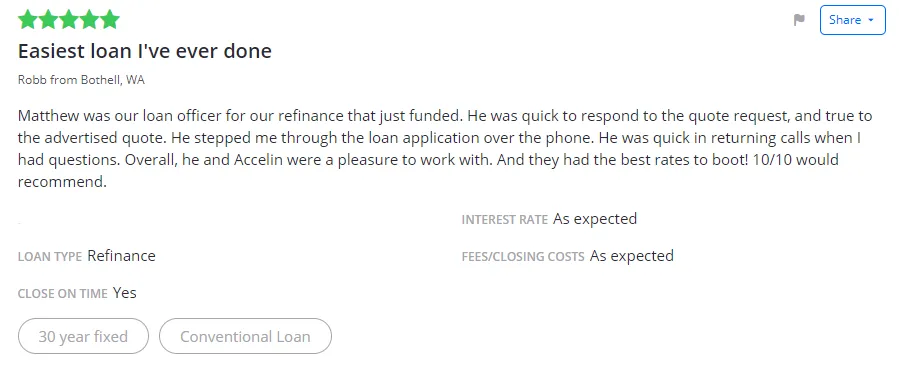

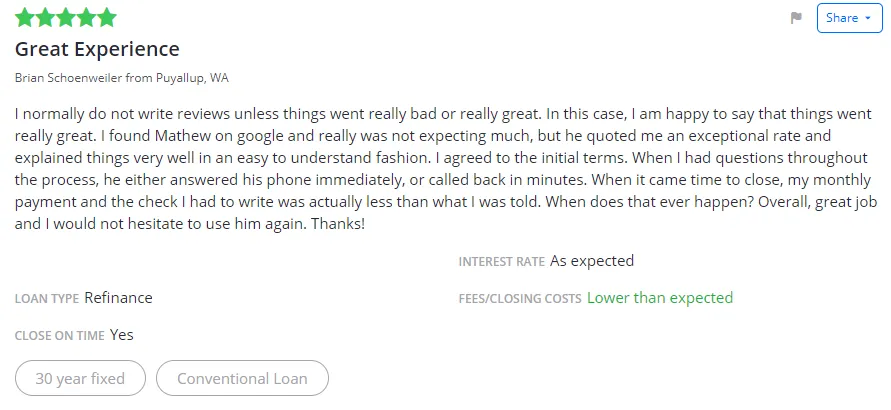

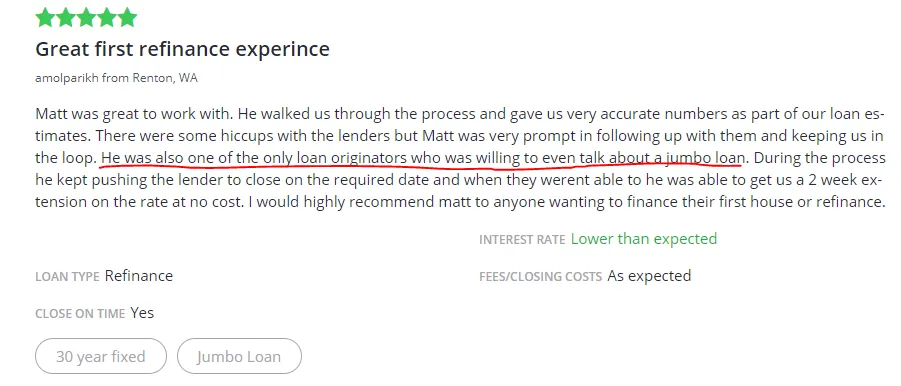

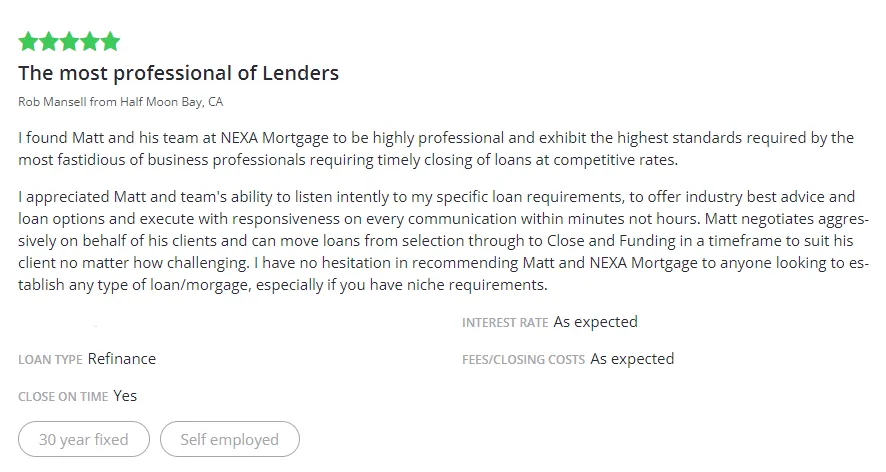

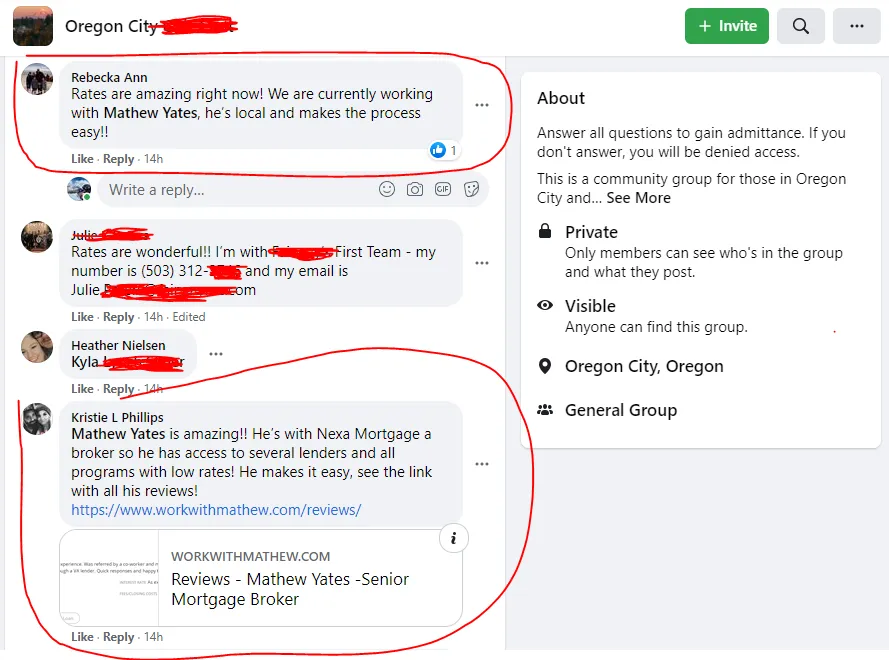

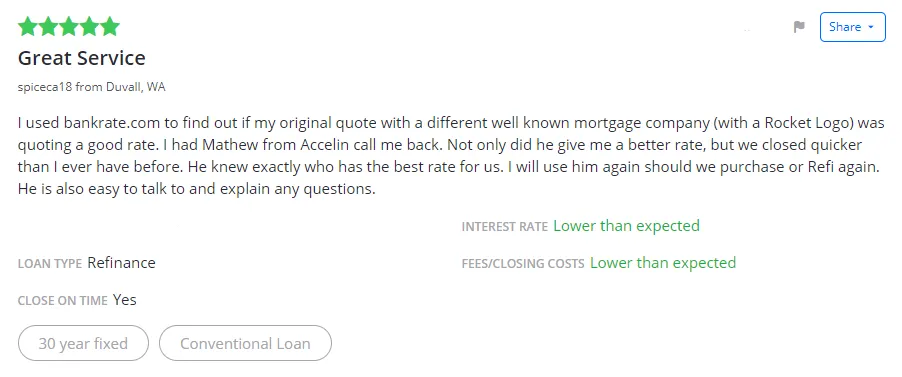

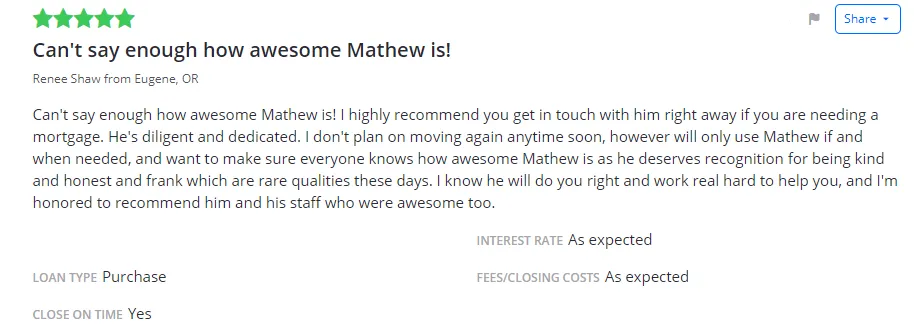

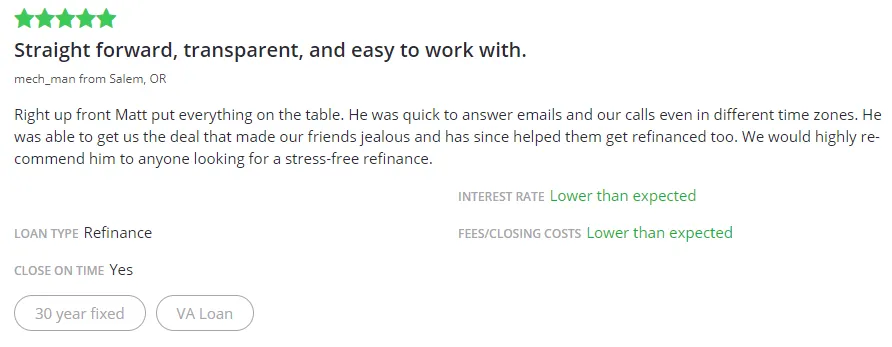

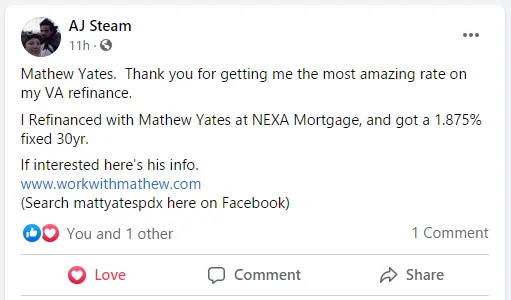

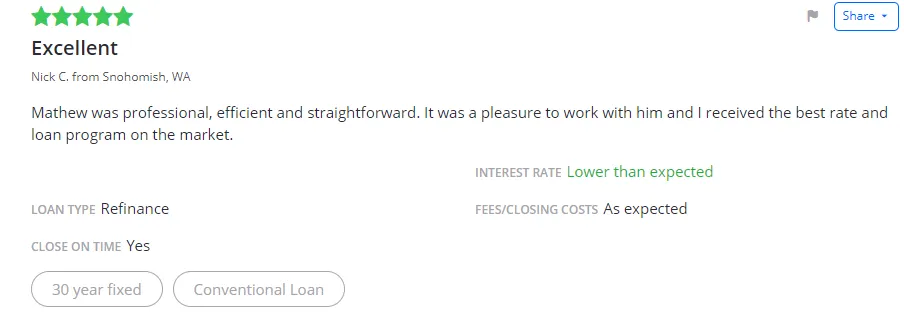

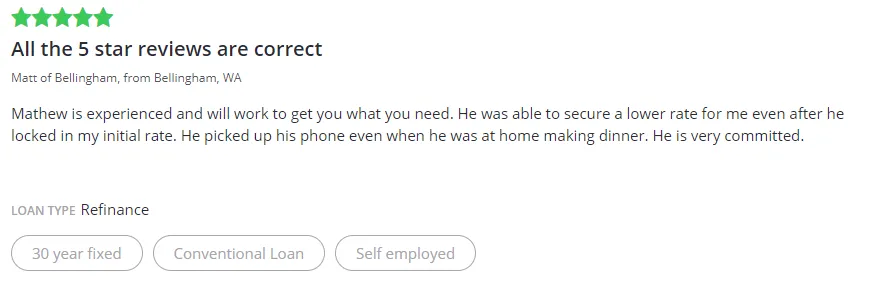

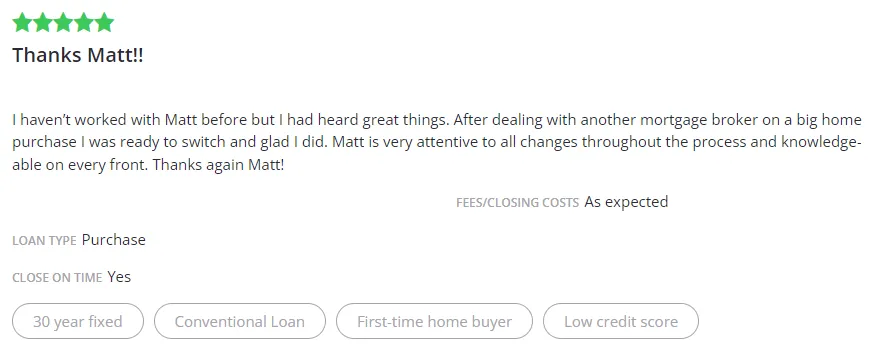

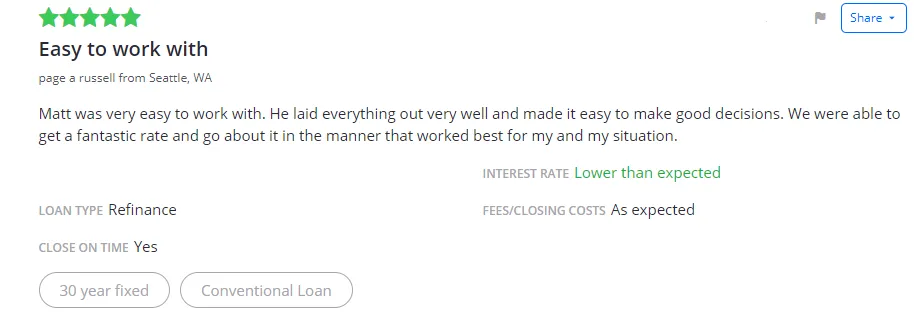

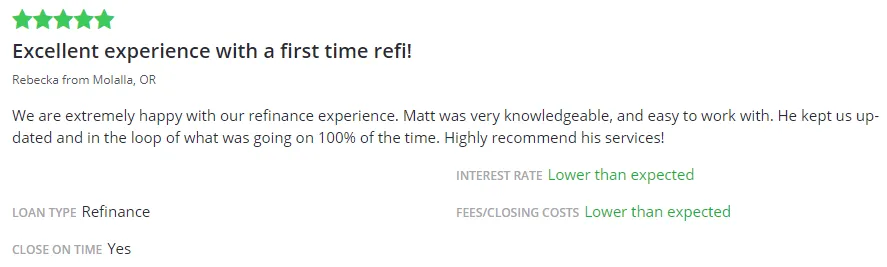

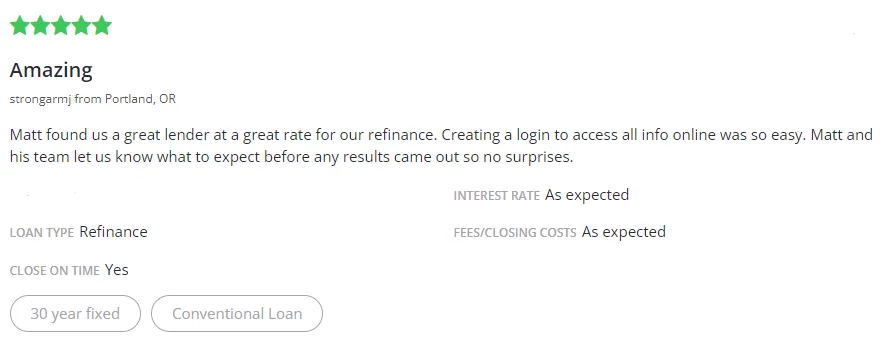

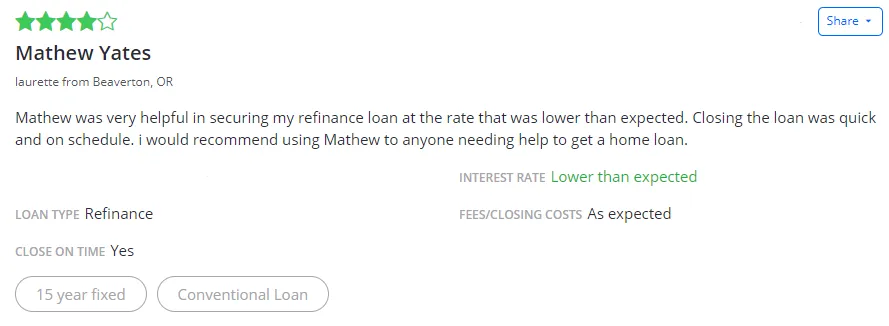

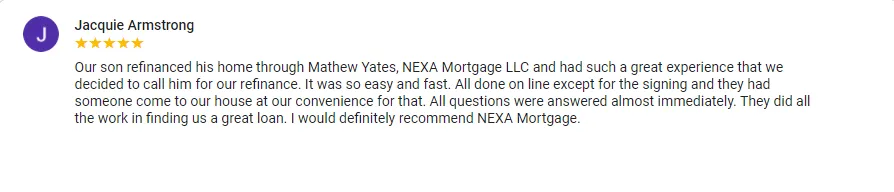

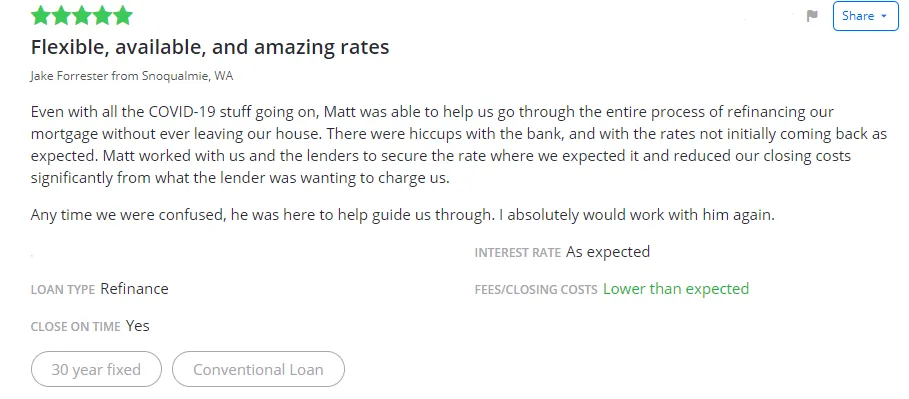

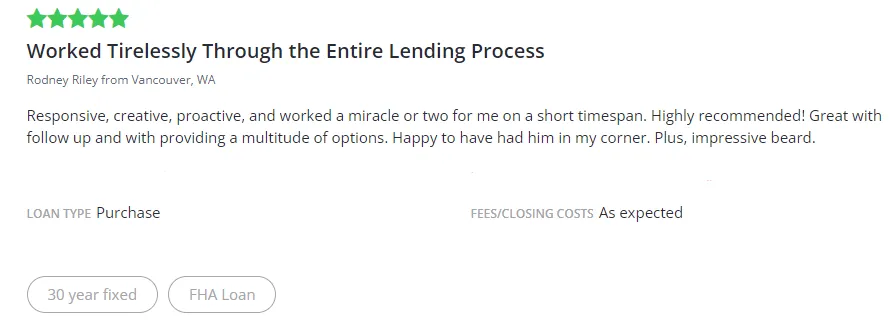

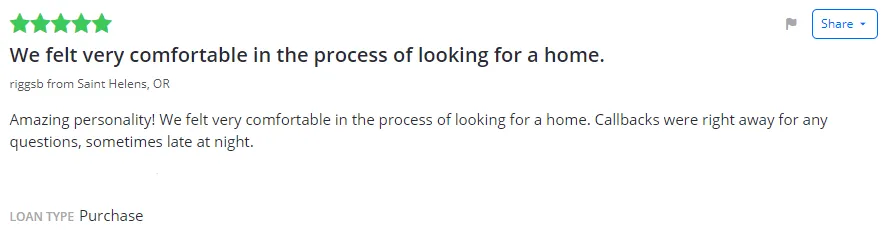

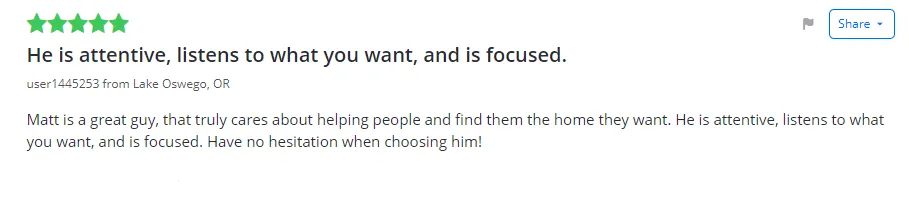

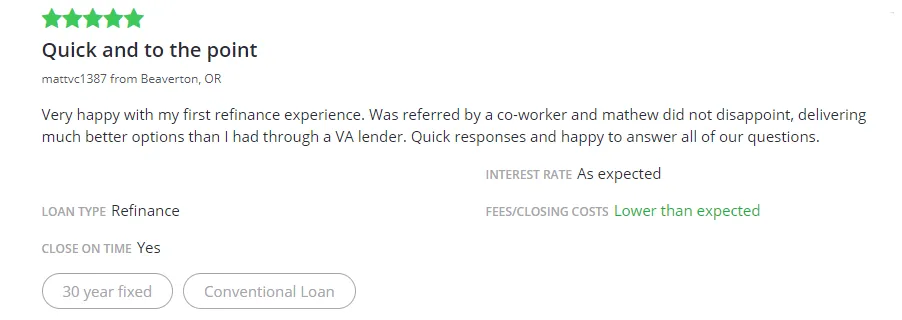

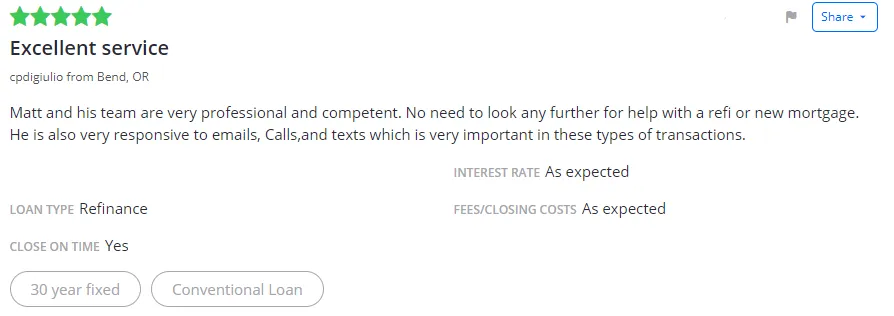

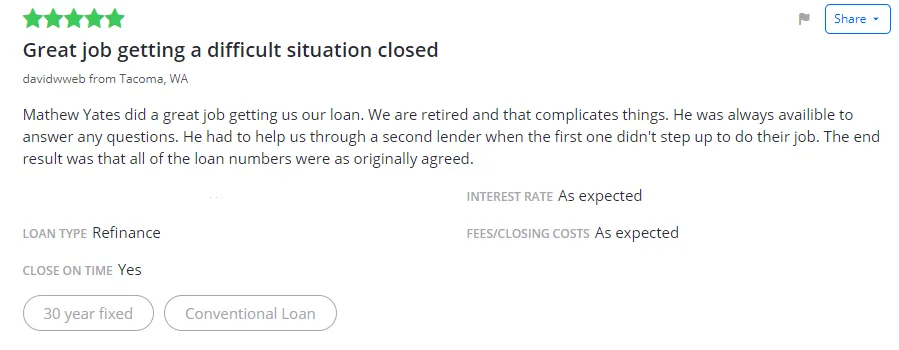

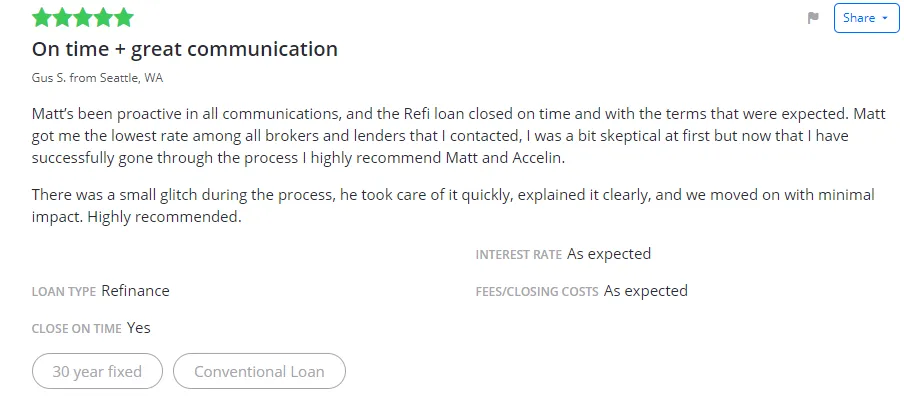

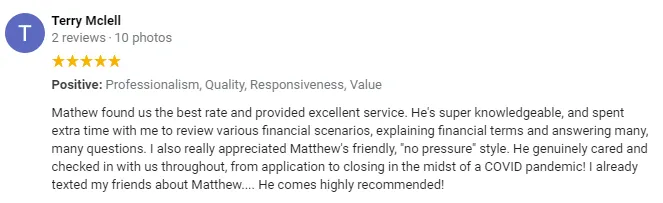

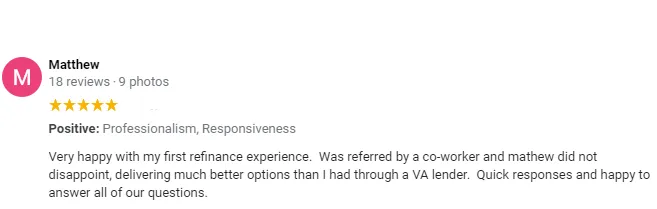

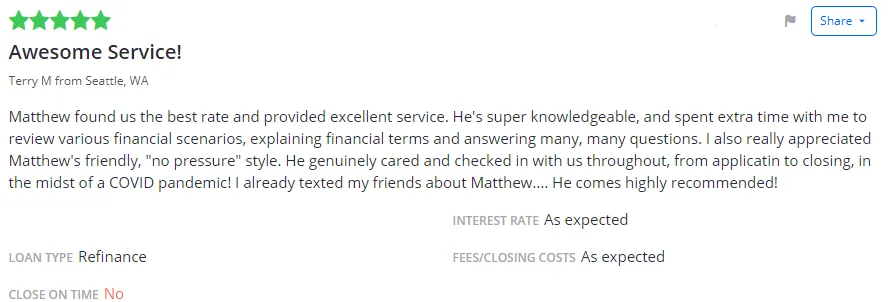

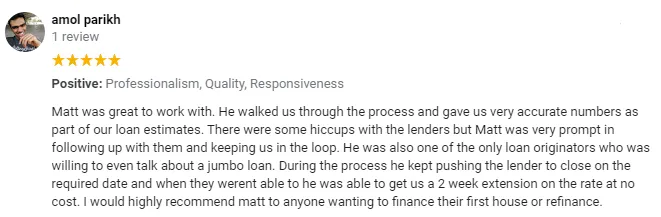

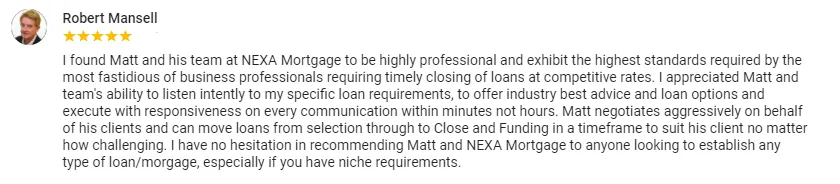

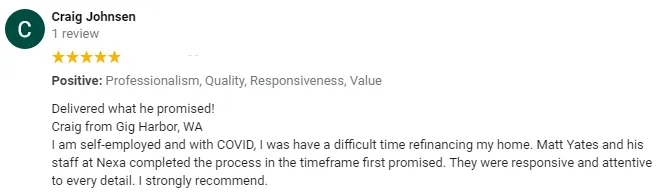

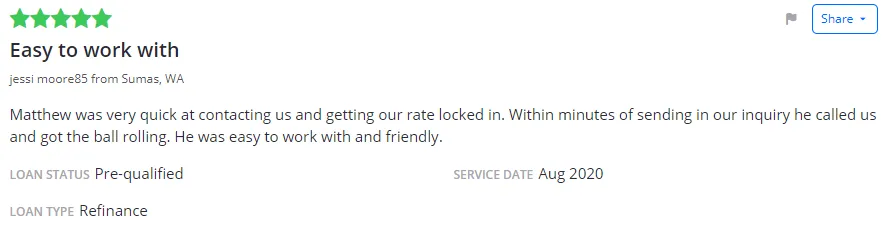

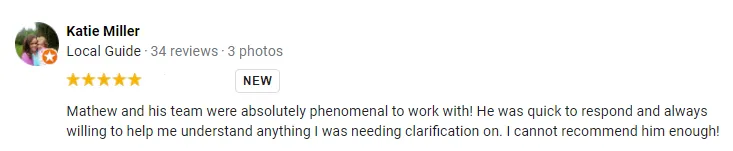

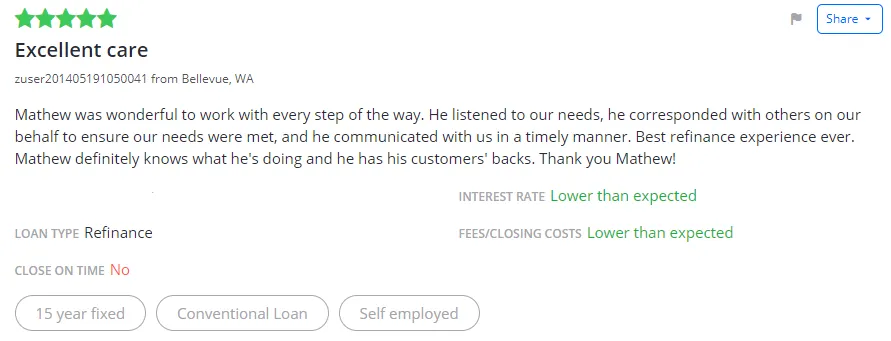

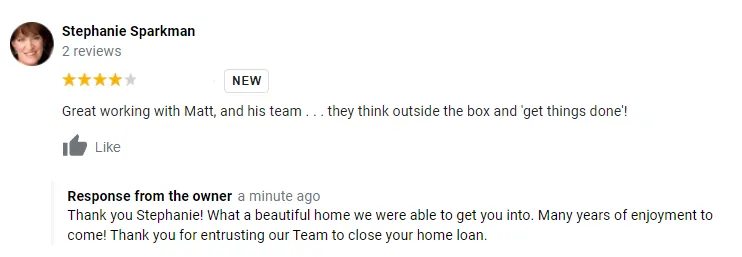

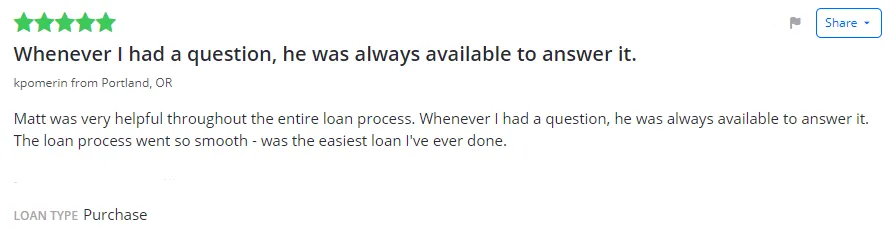

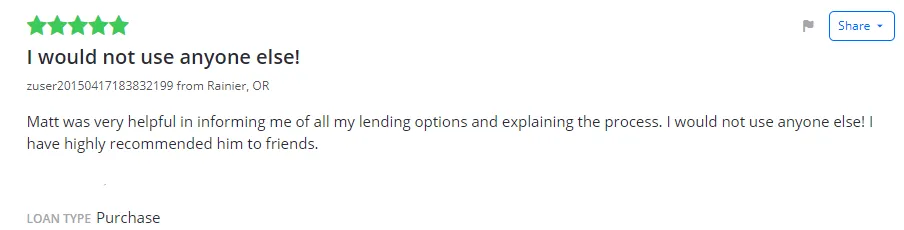

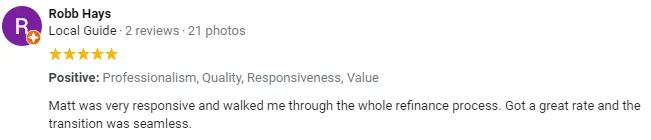

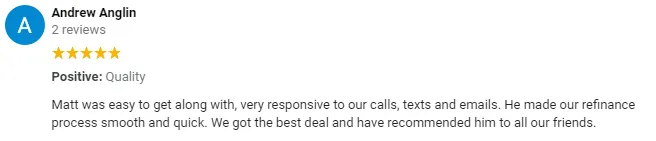

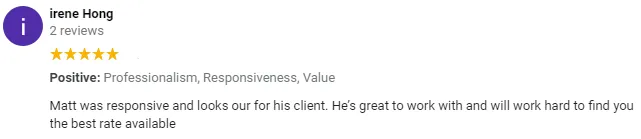

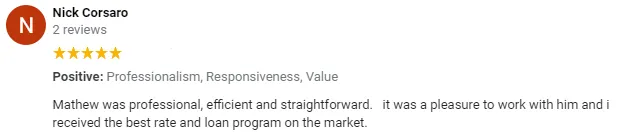

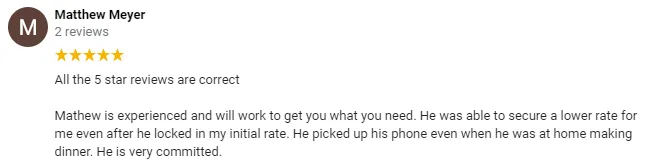

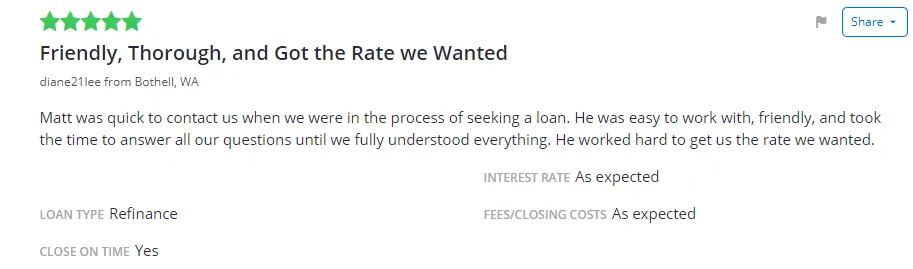

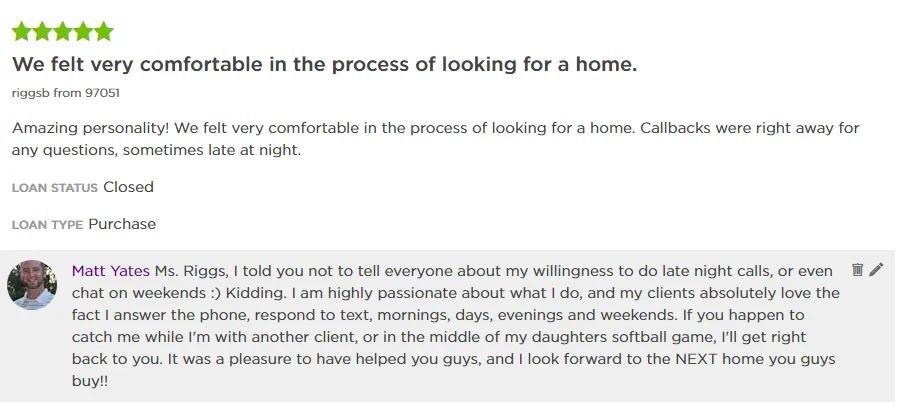

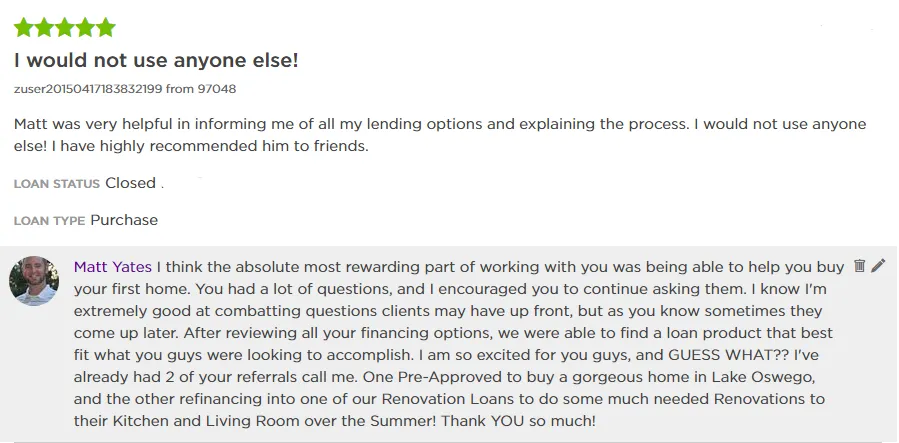

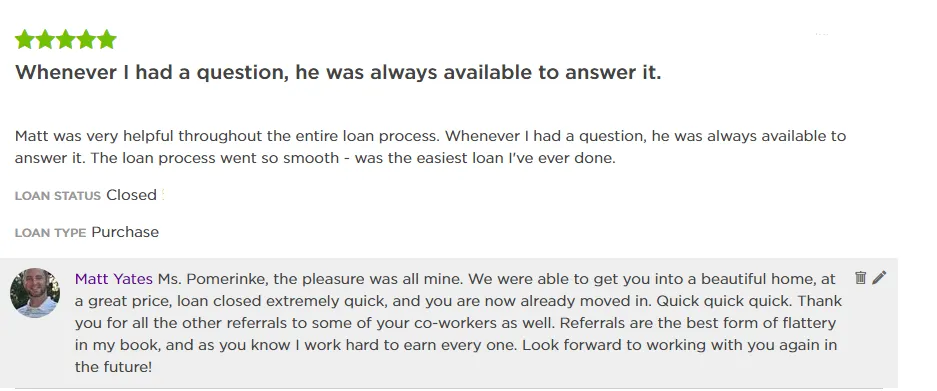

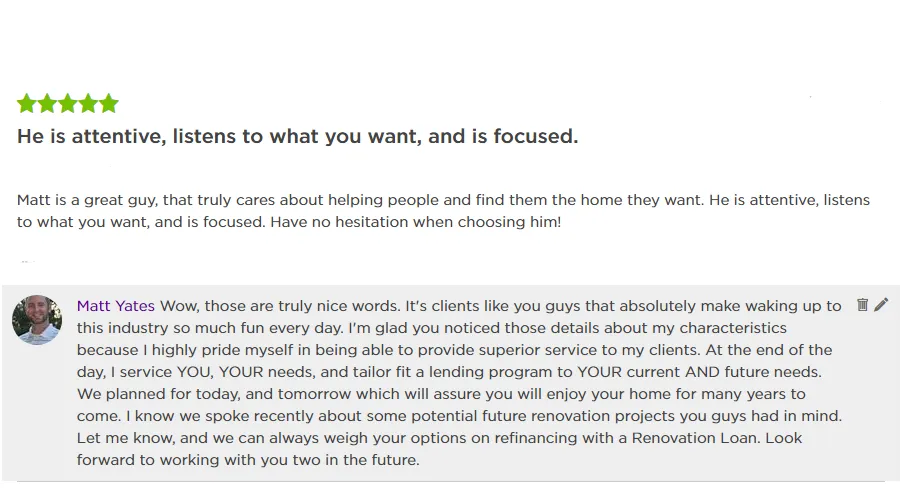

Testimonials

NMLS ID #1416824

For information purposes only. This is not a commitment to lend or extend credit. Information and/or dates are subject to change without notice. All loans are subject to credit approval. E Mortgage Capital, Inc. d/b/a E Mortgage Capital, NMLS# 1416824. Equal Housing Lender

(NMLS consumer access: https://www.nmlsconsumeraccess.org/_)